Why the Bank of England is Wrong

Interest rates, dodgy stats, and why we're (probably) in a recession

Today the Bank of England published its quarterly monetary policy report. While the Monetary Policy Committee (MPC) appears to be cautiously optimistic about inflation falling, it is still clearly quite spooked about increasing wages. It also paints a pretty grim picture about economic growth and its forecasts are showing no economic growth until 2025.

The MPC has got it wrong. It is not optimistic enough about inflation and is actually too optimistic about the state of the economy.

Inflation is moving in the right direction. Money and credit growth has collapsed. Consumer Price Inflation is much lower now than what was previously forecast by the Bank. Producer Price Inflation has also fallen and annual rates have actually turned negative which should be passed onto consumers meaning that core inflation will continue to fall. What is more, given the fact energy prices have lowered due to the energy price cap, headline inflation will also continue to fall. There have obviously been concerns about the ongoing situation in the Middle East but oil prices have now pretty much returned to where they were before the evil attack by Hamas. What is more, while wage growth has been high by historical standards, it has cooled and is projected by the Bank to decline in the medium term.

All of this means that the Bank should be more optimistic when it comes to inflation. Unfortunately it is forecasting that inflation will drop to about three per cent and tick at that point for some time. While I don’t think this will actually be the case, this shouldn’t be too much of a concern. Obviously the Bank is concerned about this because their mandate is to keep inflation at two per cent. I’ve written before (here and here) on why we should scrap inflation targeting and replace it with nominal GDP targeting. However, I think this is unlikely to happen anytime soon and so in the meantime we should change the Bank’s inflation target to around three per cent (I will probably write something on this in the near future, but here is a good report on the topic).

We should be much more comfortable with slightly higher rates of inflation if that means we can avoid the pain and misery of a recession. I have written a lot about recessions and the pain they cause. It’s the focus of my academic work and governments and central banks should do all they can to avoid them. Inflation can be painful and it does exacerbate the cost of living crisis, but that is nothing compared to the misery of a recession which leads to job losses and a fall in living standards. It is the poor and the young who suffer the most when the economy tanks and so it’s wrong to prioritise tackling inflation over avoiding a recession.

This brings us onto the next point. The Bank is not being pessimistic enough about the overall economy. It is forecasting zero growth (which is obviously not great) but I actually think we are likely to see a recession and might actually be in one right now. Manufacturing output and retail sales are down which is a very worrying sign. Perhaps most concerningly of all is the labour market. We have had a bit of a jobs miracle in the UK since the Great Recession and the labour market is tight by historical standards but it has been loosening as the unemployment rate has continued to rise. It looks as though the Sahm Rule (named after the excellent Claudia Sahm) might well apply here. In many ways it is irrelevant if the labour market is strong when compared to decades ago, the issue is that it’s loosening which would suggest we’re entering a recession or are already in one. Of course, this does not mean that we are definitely entering a recession as the Sahm Rule probably won’t hold up in every scenario, but the fact that unemployment is on the rise is definitely a bad omen.

This is why I wrote for the Evening Standard on why the MPC should have voted to lower interest rates today. Obviously it voted to keep Bank Rate at 5.25 per cent with three of the members being even more hawkish and favouring a hike. I expect this to be seen as a mistake in the near future. I have a lot of sympathy for the Bank given its mandate and the pressures it faces. However, I fear that its restrictive policy is in part driven by its desire to claw back some credibility after it dropped the ball by allowing inflation to get far too high and so is now overcorrecting. At its next meeting in December the MPC should vote to lower Bank Rate to five per cent and hit the pause button on Quantitative Tightening. Hopefully it won’t be too late by that point.

There is another issue which needs to be discussed although it is getting very little attention. Some of the data which is guiding the MPC is far less robust than it should be. I’ve written before about the danger posed to our economy by dodgy forecasts by bodies such as the ONS and it looks as though things are even worse than feared. The response rate to the Labour Force Survey by the ONS has fallen to below 20 per cent. While the ONS can still get data from HMRC this is a problem. The Labour Force Survey is incredibly useful in shining a light on the labour market and can help to explain why people are out of work.

Part of this low response rate is due to Covid as the ONS decided to call people up rather than visit them at home (for obvious reasons). However, most people just don’t pick up the phone if they don’t recognise the number. Also, completing many of the surveys is a burden for people. I have never done one but my mum did do one and it involved multiple meetings with an ONS employee and involved discussions about her wellbeing (apparently he had a strong smell of tobacco). I think the ONS does a great job and is fantastic at finding novel ways to get around these types of problems, but it urgently needs to review its practices and look at ways to incentivise participation by paying households rather than just relying on their goodwill. It’s encouraging that the Bank has brought in Ben Bernanke to review its own forecasting and the ONS should do something similar.

You Do Not, Under Any Circumstances, "Gotta Hand It To Donald Trump”

Here is something for you trade nerds, of which there are many (thanks Sam Lowe). Last week the Wall Street Journal published an op-ed praising Donald Trump’s proposal to levy a tariff of at least 10 per cent on all goods entering the US. The author argued that this would reduce the trade deficit and get America making stuff again.

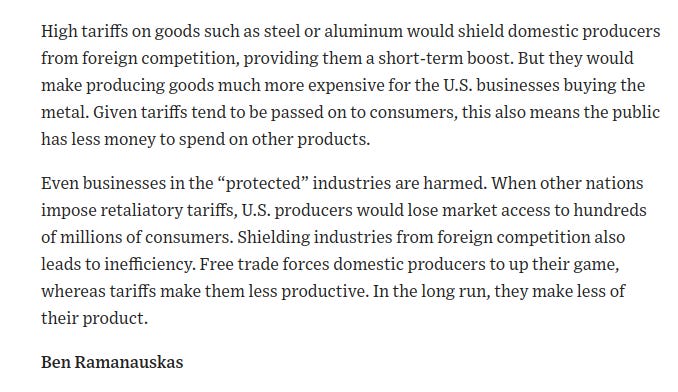

The WSJ was kind enough to publish my letter which you can read here. I explain that tariffs might offer a short term boost to some producers but that comes at the expense of firms in other industries and consumers. It is also bad for businesses in the ‘protected’ industries as they’ll likely find retaliatory tariffs slapped on their own products in other countries. Regrettably it is paywalled as the WSJ is after your dosh, but here is a screenshot of the letter

.

Supporting my work

On the topic of money, last week I pointed out that I have no intention to start charging for Opportunity Lost. However, it would be nice if this wasn’t a loss-making venture for me given that I write most of my articles from Spoons and of course it represents an opportunity cost as I could be doing something else with the time spent writing them. If you enjoy my writing then why not consider bunging some cash my way: https://www.buymeacoffee.com/opportunitylost

Thank you as ever for reading.

Ben

P.S. The Lego photo was generated by AI (inspired by Joey Politano) so sadly you can’t buy it.